Locked Box vs. Completion Accounts

Most deal teams treat the choice between locked box and completion accounts as a drafting preference.

It isn’t.

It’s a structural decision about who bears economic risk, who controls financial information, and how much trust exists between buyer and seller.

Choose the wrong mechanism—and you don’t just create friction. You embed misaligned incentives, valuation gaps, and predictable disputes into the deal itself.

This guide explains the real difference between locked box vs completion accounts, how each mechanism behaves in practice, and how to choose correctly.

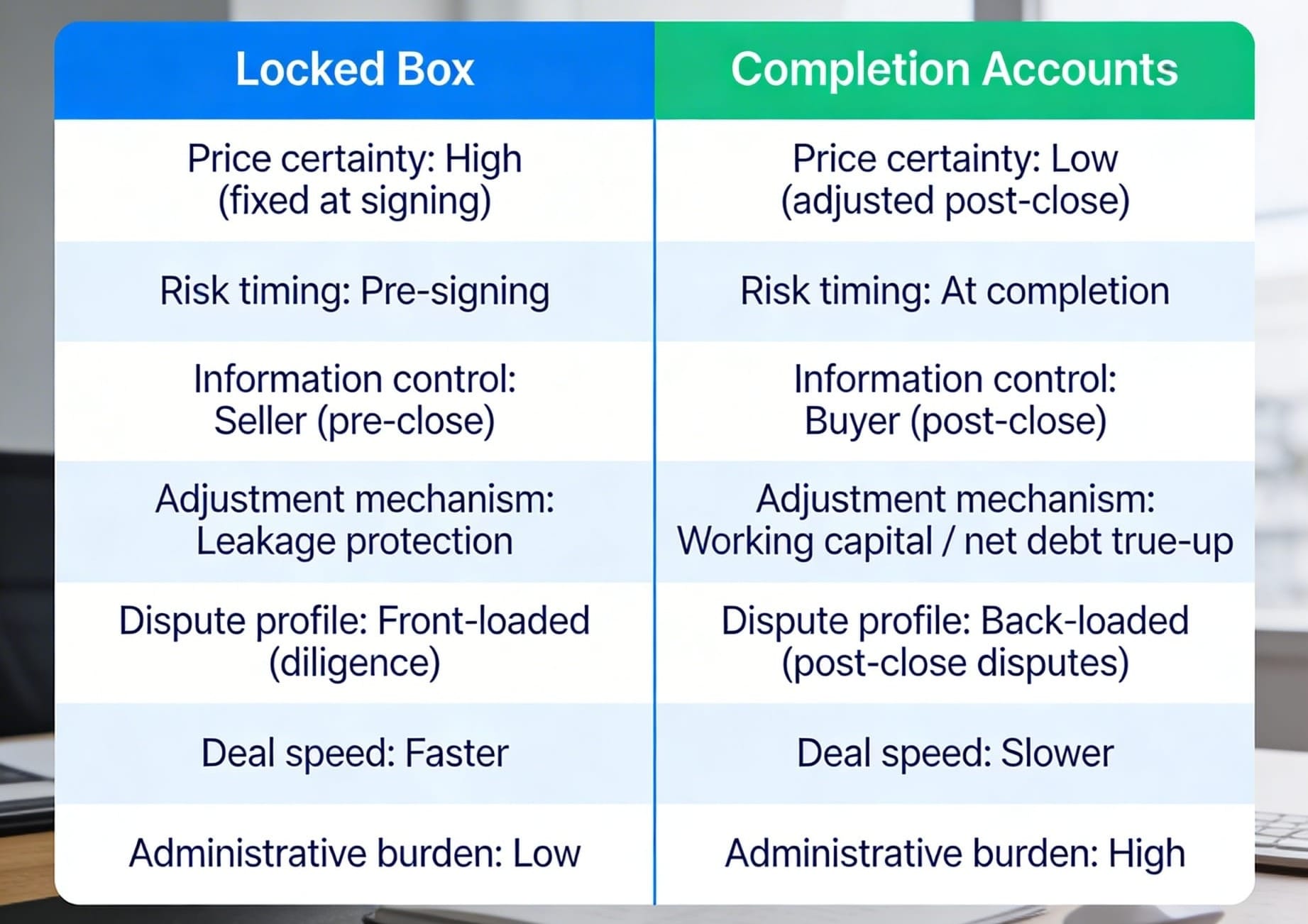

What Is the Difference Between Locked Box and Completion Accounts?

The distinction between locked box and completion accounts appears straightforward, and is typically explained in terms of timing:

- Under a locked box, the purchase price is fixed at signing by reference to a historical balance sheet, and is not adjusted following completion.

- Under completion accounts, the purchase price is determined after closing by reference to the target’s actual financial position at the moment of completion.

While accurate, this description understates the significance of the distinction.

A more useful way to understand the difference is to recognise that each mechanism embodies a different theory of what the purchase price represents:

- Under completion accounts, the price is intended to reflect the actual financial condition of the business at the point of transfer, with adjustments ensuring that the buyer pays precisely for what it receives.

- Under a locked box, the price reflects an agreed historical valuation, with the economic risk of subsequent performance—whether positive or negative—allocated to the buyer from the locked box date onward.

How Pricing Mechanisms Determine Economic Ownership

At what point does the buyer become the economic owner of the target business?

The answer to that question determines how fluctuations in working capital, trading performance, and balance sheet composition are allocated between the parties.

Completion Accounts: Economic Ownership Transfers at Completion

Under a completion accounts structure, the transaction is designed so that economic ownership and legal ownership coincide at the moment of completion, with the buyer assuming both control and risk simultaneously.

The buyer pays a provisional purchase price at closing—typically based on estimated working capital and net debt—and subsequently prepares a set of completion accounts that reflect the target’s actual financial position at that precise point in time.

The purchase price is then adjusted, often on a pound-for-pound basis, to reflect any deviation from the agreed benchmarks.

In conceptual terms, this mechanism attempts to achieve economic precision, ensuring that:

- The seller bears the risk of pre-completion trading fluctuations

- The buyer pays only for the assets and liabilities actually received

However, while the logic is compelling, it depends critically on the assumption that the actual financial position of a business at completion can be determined in an objective and uncontested manner—a premise that does not hold in practice.

Locked Box: Economic Ownership Transfers Before Completion

In contrast, a locked box structure deliberately separates economic ownership from legal ownership, transferring the former at a fixed historical date while leaving the latter with the seller until completion.

From the locked box date onward:

- The buyer is treated as the economic owner of the business

- The seller operates the business in a custodial capacity

The purchase price is fixed by reference to the locked box accounts, and is not revisited after closing, regardless of how the business performs in the interim period.

To protect the buyer, the seller undertakes not to extract value from the business during this period—other than agreed “permitted leakage”—with any unauthorised leakage typically compensated on a pound-for-pound basis.

This structure replaces post-completion adjustment risk with pre-signing diligence risk, fundamentally shifting when uncertainty must be resolved.

Why Completion Accounts Consistently Produce Disputes

Completion accounts are often perceived as a neutral, objective mechanism for determining price.

In reality, they create a framework in which disputes are structurally embedded.

Accounting Judgement and the Illusion of Objectivity

The preparation of completion accounts requires the application of accounting policies to a specific set of facts at a defined point in time, but many of the most economically significant line items are inherently judgmental.

These include:

- Provisions against doubtful receivables

- Inventory obsolescence reserves

- Accrual completeness

- Revenue recognition cut-offs

Each of these involves assumptions about future outcomes, and small changes in those assumptions can produce material movements in the purchase price.

For example, a modest increase in provisioning assumptions across multiple balance sheet categories can generate a multi-million-pound downward adjustment, even where each individual assumption is defensible in isolation.

The Ambiguity of Consistent with Past Practice

Most SPAs attempt to constrain this discretion by requiring that completion accounts be prepared “on a basis consistent with the target’s historical accounting policies.”

However, this formulation introduces its own ambiguity.

Does consistency require:

- Identical methodologies, even if circumstances have changed?

- The same level of conservatism, regardless of new information?

- Outcomes that broadly resemble historical patterns?

In practice, this phrase becomes a focal point for disputes, as it is sufficiently flexible to support competing interpretations while appearing, on its face, to impose discipline.

Post-Completion Information Asymmetry

Perhaps the most significant structural feature of completion accounts is the inversion of information asymmetry that occurs at completion.

Prior to closing, the seller controls the financial information and has superior knowledge of the business.

Immediately after closing, that advantage transfers entirely to the buyer, who now controls:

- The accounting systems

- The finance team

- The preparation of the completion accounts themselves

The seller, by contrast, must challenge those accounts from an external position, often with limited access to underlying data.

This creates a dynamic in which the party responsible for preparing the accounts is also the party that benefits from downward adjustments, making disputes not only likely but rational.

The True Cost of Completion Accounts

Even in the absence of formal disputes, completion accounts impose a significant burden on both parties.

The buyer’s finance team must dedicate substantial resources to preparing the accounts during the critical post-acquisition integration period, while the seller must engage advisers to review and, where necessary, challenge the outcome.

Where disagreements arise, the process can extend over several months, with costs that are material relative to the size of the adjustment itself.

The Locked Box Mechanism: Certainty with Different Risks

The locked box mechanism addresses many of the inefficiencies associated with completion accounts by eliminating post-completion price adjustments altogether.

However, in doing so, it introduces a different set of risks that must be carefully managed.

The Problem of Staleness

Because the locked box relies on historical accounts, there is inevitably a gap between the locked box date and completion.

During this period:

- The buyer bears economic risk

- The seller retains operational control

If the target’s financial position deteriorates during this interval—whether due to seasonality, market conditions, or operational issues—the buyer has no recourse through the pricing mechanism.

This risk is particularly acute in businesses with volatile or unpredictable working capital dynamics, where historical snapshots may not accurately reflect current conditions.

Leakage and Its Boundaries

The primary protection afforded to the buyer is the leakage covenant, which prohibits the extraction of value from the business between the locked box date and completion.

While conceptually straightforward, the distinction between prohibited leakage and permitted leakage is often less clear in practice.

Issues commonly arise in relation to:

- Intra-group transactions conducted on purportedly arm’s-length terms

- Management compensation that may straddle the boundary between ordinary course and deal-related incentives

- Adjustments to transfer pricing arrangements

As a result, disputes under locked box structures tend to focus not on whether value has left the business, but on how that value should be characterised.

Incentive Misalignment in the Interim Period

The separation of economic and legal ownership creates a form of incentive misalignment during the period between signing and completion.

The seller, no longer benefiting from the future performance of the business, may have reduced incentive to:

- Invest in growth initiatives

- Optimise working capital

- Make discretionary expenditures

While conduct-of-business covenants are intended to mitigate this risk, they cannot fully replicate the incentives of true economic ownership.

The Central Role of Due Diligence

Because the purchase price cannot be adjusted post-completion, the locked box mechanism places significant emphasis on the quality of pre-signing due diligence.

Buyers must achieve a high degree of confidence in:

- The accuracy of the locked box accounts

- The sustainability of working capital levels

- The appropriateness of accounting policies

Any deficiencies in these areas cannot be corrected through a price adjustment, and instead become matters for warranty and indemnity claims, which are inherently more complex and constrained.

Choosing the Right Mechanism: A Commercial Framework

The decision between locked box and completion accounts should be driven by a structured assessment of the transaction’s underlying characteristics.

Four factors are particularly relevant.

1. Financial Stability of the Target

Where the target exhibits stable, predictable financial performance and limited working capital volatility, a locked box structure is generally more appropriate.

Conversely, where financial performance is volatile or highly seasonal, completion accounts provide a mechanism for aligning price with actual outcomes.

2. Quality and Transparency of Financial Information

Locked box structures rely on high-quality, reliable financial information at the locked box date.

Where such information is unavailable or subject to uncertainty—as is often the case in carve-out transactions—completion accounts may be preferable.

3. Deal Process Dynamics

In competitive auction processes, the locked box facilitates bid comparability and reduces execution risk, making it attractive to sellers.

In bilateral negotiations, where such considerations are less pressing, completion accounts may be more acceptable to both parties.

4. Allocation of Risk and Negotiating Leverage

Ultimately, the choice of mechanism reflects a negotiation over risk allocation.

- Sellers typically prefer locked box structures, which provide price certainty and a clean exit

- Buyers often prefer completion accounts, which offer protection against adverse developments

The agreed mechanism reflects the relative bargaining power of the parties and their respective appetites for risk.

The Emergence of Hybrid Structures

In practice, an increasing number of transactions adopt hybrid approaches, combining elements of both mechanisms to address specific areas of uncertainty.

For example:

- A locked box may be used to fix the core valuation

- Limited post-completion adjustments may be permitted for defined items, such as net debt or contingent liabilities

These structures reflect a broader trend towards bespoke risk allocation, rather than reliance on binary choices.

Final Takeaway

Neither locked box nor completion accounts eliminate uncertainty.

They simply determine:

- when that uncertainty is resolved

- who controls the relevant information

- who ultimately bears the economic consequences

Completion accounts defer uncertainty until after closing, placing it in the hands of the buyer.

The locked box requires that uncertainty be addressed before signing, through diligence and pricing.

The correct choice, therefore, is a matter of commercial judgment:

Which party is better positioned to understand, manage, and absorb the risks inherent in the transaction?

Case Study: How Pricing Mechanism Choice Created a £3M Dispute (and How It Could Have Been Avoided)

To illustrate how these mechanisms behave in practice, consider a mid-market private equity exit involving a UK-based manufacturing business.

Transaction Overview

- Enterprise Value: £85 million

- Seller: Private equity sponsor

- Buyer: Strategic acquirer

- Structure: Completion accounts

- Target working capital: £6.5 million

At signing, both parties agreed that completion accounts would provide a fair and precise adjustment mechanism, particularly given the buyer’s concern about working capital variability.

On paper, the choice appeared entirely reasonable.

In practice, it produced exactly the type of dispute the mechanism is structurally predisposed to create.

What Happened Post-Completion

Following completion, the buyer prepared the completion accounts and proposed a £3.2 million downward adjustment to the purchase price.

The adjustment was driven primarily by three items:

- Receivables provisioning

- Buyer increased bad debt provision assumptions based on post-completion collections data

- Seller argued this was inconsistent with historical provisioning methodology

- Inventory valuation

- Buyer applied a more conservative obsolescence reserve

- Seller argued inventory had historically turned without issue

- Accruals for supplier liabilities

- Buyer recognised additional costs not previously accrued

- Seller claimed these related to post-completion decisions

Individually, each adjustment could be defended.

Collectively, they produced a material reduction in price.

Why the Dispute Escalated

The disagreement did not arise because either party was acting irrationally or in bad faith.

It arose because the mechanism itself created conflicting incentives and interpretive ambiguity.

1. Competing Views of Consistency

The SPA required accounts to be prepared on a basis “consistent with past practice.”

- Buyer’s interpretation: apply the same principles, updated for new information

- Seller’s interpretation: replicate historical outcomes and assumptions

This difference in interpretation became the central point of contention.

2. Information Asymmetry After Completion

By the time the dispute arose:

- Buyer controlled all financial data and systems

- Seller had limited visibility into underlying assumptions

The seller was effectively challenging a set of accounts prepared by a party with both informational advantage and economic incentive.

3. Timing and Leverage

The seller, having already distributed proceeds to investors, faced:

- Immediate pressure to resolve the dispute

- Limited appetite for prolonged expert determination

The buyer, by contrast, could sustain a longer process.

This imbalance influenced negotiation dynamics.

Outcome

After four months of negotiation and partial expert involvement:

- The parties agreed on a £1.9 million reduction

- Combined advisory costs exceeded £400,000

While the dispute was ultimately resolved, the process:

- Delayed value certainty

- Consumed management attention

- Introduced avoidable friction into the transaction

Counterfactual: What If This Had Been a Locked Box Deal?

Had the same transaction been structured as a locked box:

- The £3.2 million adjustment dispute would not have arisen

- Price would have been fixed at signing

- The buyer would have borne the risk of working capital deterioration

However, this would have shifted the burden elsewhere:

- The buyer would have needed to diligence:

- Receivables quality

- Inventory turnover

- accrual completeness

- Any concerns would need to be reflected in price before signing, rather than argued after completion

In other words:

The dispute would not have disappeared - it would have been resolved earlier, through pricing rather than process.

- Completion accounts → resolve disagreement after closing, through negotiation

- Locked box → resolve disagreement before signing, through diligence and pricing